Researchers say 82% of businesses fail because of cash flow management problems.

This article can serve as a guide, helping you to improve your ecommerce accounting system. Learn the difference between accrual and cash-basis accounting, choose the right type of business account, and tap into accounting best practices. You’ll even learn how to pick the best accounting software for your ecommerce business.

Key takeaways

- Ecommerce accounting is a crucial business component involving the organization of financial data and filing of financial reports.

- Business owners can choose between accrual or cash basis accounting for their ecommerce company.

Ecommerce accounting basics

Imagine you’ve launched a booming ecommerce company. You’re ordering supplies, filling orders, and taking payments every single day. Ecommerce accounting involves recording and maintaining all the financial data involved with your company.

Ecommerce accounting is slightly different than the accounting you’d do in a brick-and-mortar store, as all the work happens online. Your customers may place orders and wait for them, payments may hang with a processor before you get them, and shipping costs could add to your expenses. Ecommerce accounting tracks all of these disparate data points.

Ecommerce accounting involves tracking these things:

- Money moving into and out of your business

- Gross margins, defined as your revenue minus your expenses

- Profits earned and losses sustained

You’ll also be responsible for interpreting the tax code and paying all the state, local, and regional taxes owed by your company. Tracking all those changes isn’t easy—in 2019 alone, standard sales tax rates changed 619 times.

Creating financial reports can be time-consuming, but the more precise you can be, the better you’ll understand your current business and your plans for the future.

Different types of business bank accounts

To give and receive money, ecommerce business owners need bank accounts. To protect your profits and plan for the future, you might need different types of financial tools. As a business accountant, you’ll need to manage movement into and out of all of these accounts and manage financial statements for all of them.

Some experts say individuals should have four different accounts. Some businesses might need more or less depending on their unique needs and specific industry.

Four common business account types exist:

- Checking accounts: These bank accounts can both accept money and send it back out again. You’re typically not required to keep a minimum in a checking account, but you rarely make money through interest payments. Some checking accounts limit how many transactions you can make each month.

- Savings accounts: These bank accounts serve as secure spots into which you can transfer money from a commonly used checking account. This can help you weather a financial storm, and allow you to earn interest on balances you carry from month to month. However, keep in mind that you can’t make multiple withdrawals from this account type each month.

- Money market accounts: These less common business accounts combine the benefits of checking and saving accounts. They offer the advantage of higher interest rates, but may require you to maintain a minimum balance. Some money market accounts come with flexibility, allowing you to write checks, use an ATM, and more.

- Merchant accounts: Think of a merchant account as a holding area for your debit and credit card payments. Customers put money here, and it goes into your business accounts later. These accounts are often tied to one- or three-year contracts.

Cash basis & accrual accounting

Business accounting means tracking money coming in and money coming out. But when do those data points enter your ledger? Two types of accounting for business exist: cash based and accrual.

In accrual accounting, you’ll make a record each time you make a sale. It doesn’t matter if your bank’s ledgers have recorded a deposit or withdrawal. As soon as the sale happens, you make a record.

In cash-based accounting, you’ll make a record based on activity in your bank account. When the money hits or leaves, you ensure your books match those of your bank.

Both methods involve tracking shipping costs. These are your expenses, and they have a deep impact on your profits. But the accounting system you choose will determine when you record sales, shipping, and other transaction details.

How to do accounting for ecommerce

Bookkeeping tasks aren’t popular — 40% of small business owners say this is the worst part of owning their companies. But working with a contractor isn’t always the answer. Many business owners don’t understand the financial reports created by their accountants.

Understanding bookkeeping tasks can help you make smart business decisions for your ecommerce store—whether you’re doing the work yourself or hiring a bookkeeping service.

Categorize transactions & spending

Ecommerce companies churn out two main types of transactions every day: income (or money coming in through purchases) and expenses (or money spent on payroll, shipping, or product). Your financial data should be categorized accordingly.

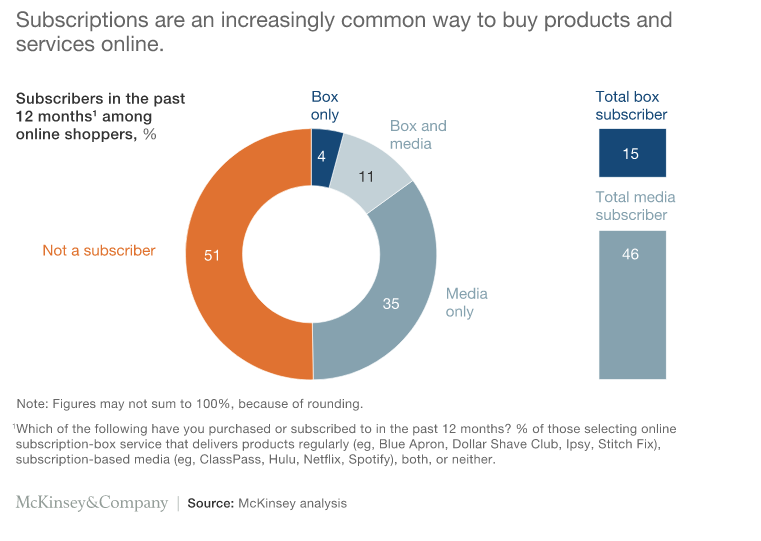

With subscription ecommerce businesses, customers may be charged before products have shipped, which should also be taken into account.

Accounting software solutions can help you manage transactions, whether they’re happening spontaneously or on a set schedule. Some interface directly with your bank accounts to automatically import data, and you can categorize accordingly.

Track chargebacks & customer returns

Customer returns are frustratingly common. In 2021, about 16.6% of products were returned, and experts think the number will rise due to online sales. Chargebacks happen often, too. When card users tell their companies the charges aren’t valid, the companies come to you for a refund.

Both chargebacks and customer returns aren’t technically revenue. You didn’t earn this money. But the funds can hit your account and cause balance sheet issues and liabilities if not recorded properly.

You must watch for them on bank statements and ensure you’re marking them (and any associated fees) properly.

Monitor expenses

Every business spends money to make money. These transactions must show up as part of your recordkeeping work.

Your ecommerce expenses might include the following:

- Shipping costs

- Vendor fees

- Marketing costs

- Business taxes paid

- Sales taxes paid

You’ll need receipts for all of these expenses, so you’ll have everything ready to go when tax season rolls around. Some forms of accounting software allow you to attach electronic receipts to each transaction, making tracking data for your tax return much easier.

Manage inventory & inventory cash flow

How many products do you have sitting on shelves, waiting to get sold? If you make your products, how much have you spent on raw materials that are waiting to get transformed by your staff? These two data points represent your inventory and your inventory cash flow.

An inventory cash flow statement can help entrepreneurs understand whether they need to order more raw materials to meet demand. And if your inventory is high, a sale could be looming in the company’s future.

Some software packages allow for perpetual tracking, so your sheets get updated automatically when orders come in and go out. But some companies use periodic tracking and audit their supplies periodically.

Maintain a business budget

In 2020, 21% of American households had no money set aside for an emergency. Plenty of new business owners can relate. Without a business budget, your company has no idea how much it has now and what might happen if everything goes wrong.

A business budget can help you mitigate understocking or overstocking problems. You can also determine when to move money between bank accounts to ensure you have enough to cover shortfalls.

Budgets go much deeper than bank statements. Instead of determining where you are now, a budget can help envision the future for your company.

Compute break-even sales

How many sales do you need to make a profit or just break even? Both you and the IRS will be very interested in this data point when tax time comes around.

In your tax return, you’ll need to list whether you made a profit since that amount will be taxed. Ecommerce companies that don’t track profits and losses can’t provide accurate data come tax time.

Useful bookkeeping software to try

Managing business expenses for even a small online store isn’t easy. Bookkeeping software can help you understand where you are now and what the future holds. The automation involved in most of these tools can be very helpful.

Some popular providers to look into include:

For more options, you can also browse accounting and bookkeeping software in the app store of your ecommerce platform.

Best practices for ecommerce accounting

Don’t be intimidated by ecommerce accounting. With a little practice and some diligence, you can handle all tasks like a pro and provide income statements that can guide your business. These are a few points to keep in mind:

Automate when you can

Let your accounting system do the heavy lifting for you. Don’t track business expenses by hand or rely on your memory. Allow the technology to input data where needed and track the work for you.

Reconcile often

You could print out income statements from the software and call it good. But it’s best to check the automation regularly and ensure that nothing is missed. Create a schedule that works for you and your business and stick with it, month in and month out.

Prepare for tax season

Many companies face a bill at the end of the year despite all of their forecasting work. Ensure that you have enough set aside in one of your accounts to cover your projected taxes. Make sure to include a buffer in case you must pay more than you expected.

Streamline the accounting processes for your ecommerce business

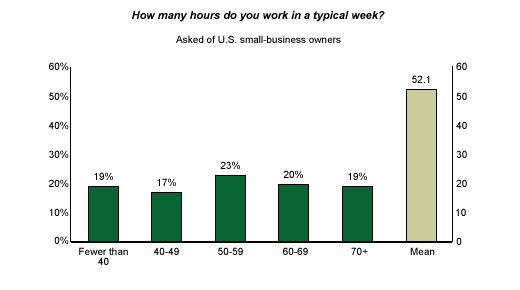

Owning a business is hard work, and many entrepreneurs spend far too many hours on the job.

Accounting and bookkeeping are crucial tasks, but few business owners have spare time to dig deep into data and really understand what’s happening with their accounts. Investing in software that can help is smart.

If you’re overwhelmed with running accounting apps, know you can hire professional accountants to help. Give them access, and they can work inside your software solutions. Meanwhile, you can log on when you need to and track progress as it happens.

Whether you outsource or use an in-house CPA, your online business may be better with an expert’s help.

FAQs on accounting for ecommerce

What is a debit?

In accounting terms, a debit is an entry recorded when a payment is made or owed to your business. Each one should be recorded in your books.

What are the benefits of inventory accounting?

Your inventory represents money waiting to be made. If you have too much of it, your prices might be too high or your marketing plan could be too weak. If you have too little inventory, you could face big problems when the orders come in.

By doing accurate inventory accounting, you can manage how much inventory you’re holding back or creating to keep your customers satisfied. Essentially, inventory accounting ensures better management of your product, so you can maximize your bottom line.

How do I prevent cash flow problems in my ecommerce business?

Business can be unpredictable, but a firm grasp of accounting can help you ride out the tide. Ensure that you control your inventory tightly, so you don’t have too much stock waiting to head out the door. And pull money out of your checking account into savings tools, so you’ll always have some on hand in case of an emergency. With strategic management, you’ll stay in a solid financial position.

Sources

[1] The Key to Managing Profit and Cash Flow for Your Small Business and Knowing the Difference Between the Two (The Hartford)

[2] New Sales Tax Report Shows a Decrease in Rate Changes in 2018 (Business Wire)

[3] How Many Bank Accounts Should You Have? An Expert Says 4 is the Magic Number (Insider)

[4] New Infographic: The Burden of Small Business Accounting, Taxes, and Payroll (PR Newswire)

[5] The Reason Most Entrepreneurs Hate Accounting (Is Not What You Think) (Forbes)

[6] Thinking Inside the Subscription Box: New Research on e-Commerce Consumers (McKinsey and Company)

[7] A More Than $761 Billion Dilemma: Retailers' Returns Jump as Online Sales Grow (CNBC)

[8] Survey: Nearly 3 Times as Many Americans Say They Have Less Emergency Savings Versus More Since Pandemic (Bankrate)

[9] Work Is a Labor of Love for Small-Business Owners (Gallup)