When it comes to mobile commerce, businesses should look at mobile payments as a must-have to remain competitive. Businesses that don’t adopt mobile payments will almost certainly lose customers.

Key takeaways

- The adoption of mobile payments is fueled by smartphone uptake, high-speed mobile data networks, and the growth of ecommerce.

- Mobile payments continue to get faster, cheaper, and more transparent.

- Improved digital wallets and other mobile payment apps are constantly emerging.

Introduction to mobile payments

Mobile payments involve the transfer of money using a phone or tablet. This practice was initially adopted in Asia and Europe before becoming more popular in North America.

In 2014, PayPal and Apple Pay introduced mobile payments by incorporating a barcode that could be scanned using a store’s barcode reader. Further developments allowed their systems to accept payments by tapping mobile devices on a contactless credit card terminal.

Some consider this contactless payment method an effective replacement for carrying physical debit or credit cards. It’s faster, more reliable, and more secure than traditional payment methods.

With the growing popularity of ecommerce, digital payments have become an acceptable way to transact business. Many stores have even integrated their point-of-sale (POS) systems with mobile payment applications.

How do mobile payments work?

Mobile payments are predicted to have a bigger market share in the years to come. By 2024, it’s projected that mobile commerce will account for nearly 43% percent of ecommerce volume, thanks to the growing number of mobile users. This growth rate can be mostly attributed to the convenience mobile payments afford consumers.

Mobile payment solutions work differently depending on the type of technology they use. Mobile wallets require downloading a third-party app. When making mobile payments in-store, the shop must have an appropriate payment processor that allows them to receive transfers.

Online shops that accept global payments can also accept transfers via mobile wallets with minimal transfer fees. These mobile wallets often use biometrics to keep the account secure.

Another type of mobile payment technology that has gained popularity in recent years is the quick response (QR) code. These codes can be customized to contain different kinds of data or identifiers. Some businesses, specifically online shops, place QR codes on the checkout page to direct customers to their payment channels. Mobile wallets can be used simultaneously with QR codes, allowing consumers to scan the merchant’s QR code to confirm the payment.

Mobile payment trends to watch in 2023

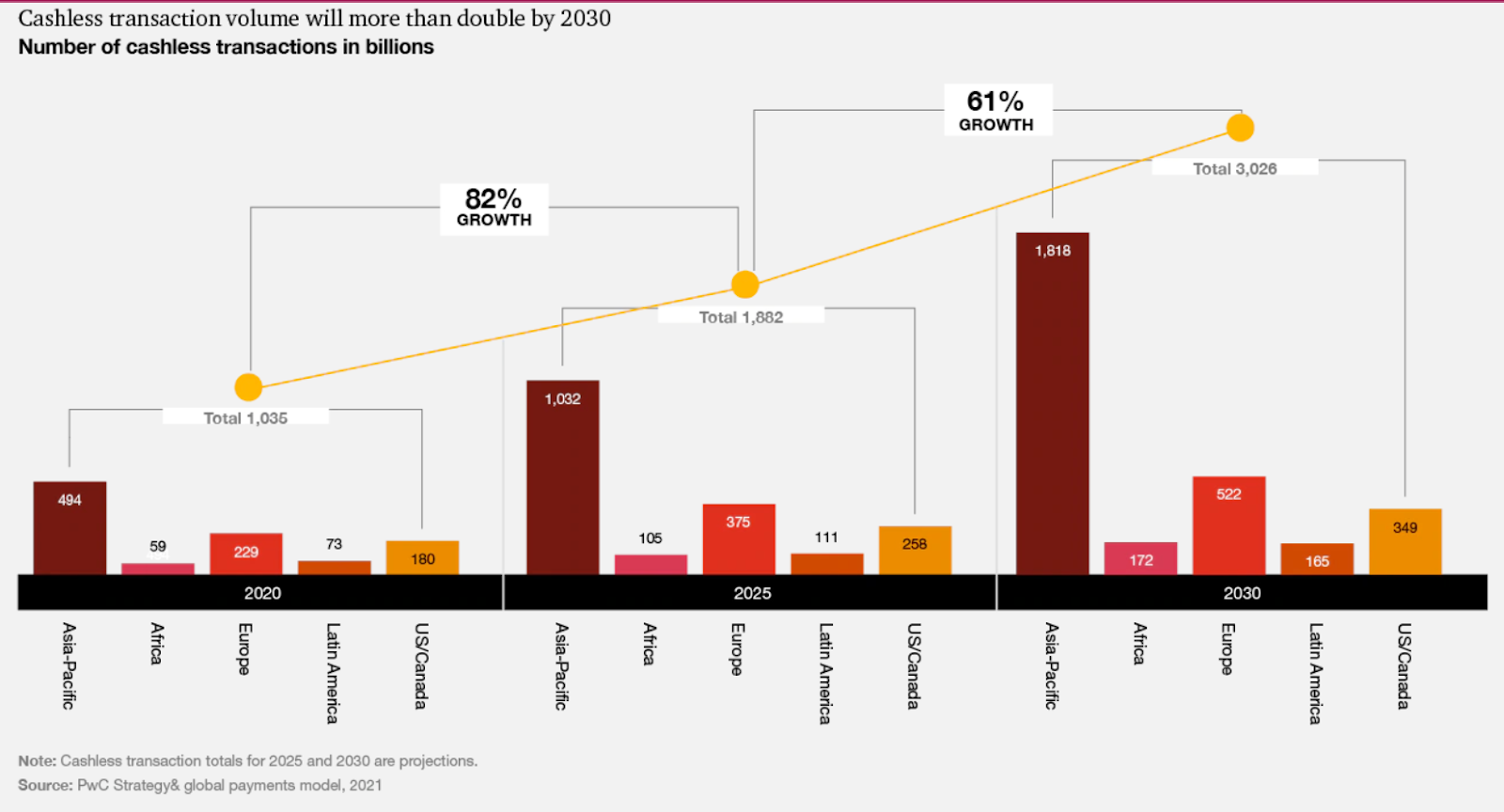

The rise of digitalization has paved the way for different financial services to become widely available. According to a report by PwC, 86%of respondents agree that traditional banking companies will partner with fintech and tech providers as a main innovation source. Cashless payments may very well become the norm, as the practice is predicted to double by 2030.

This will likely lead to several new mobile payment trends shaping the industry, including:

Mobile wallets

According to forecasts, the mobile wallet market size is expected to hit $16.2 trillion by 2031, as adoption in rural areas across the world increases.

The popularity of mobile wallets can be mainly attributed to their ease of use. Users only need to download a mobile app and supply their bank account details. After identity verification, users can make purchases right away, both in-person or online.

Mobile wallets use near-field communication (NFC), technology which allows data to be sent over very short distances, to enable contactless payments through mobile payment apps.

Tap-to-pay with contactless credit cards

While credit cards provide fast and secure payments, contactless credit cards take these benefits to a new level. To complete the transaction, a credit card equipped with a chip is tapped over a payment terminal, and NFC is used to transfer data wirelessly.

With this technology, the payments system generates a code specific to a credit card and the transaction being made. This single-use-only code provides an added layer of security because the bank is the only entity that can decode it to verify the transaction.

More P2P payments

Peer-to-peer (P2P) transactions will likely soar in the near future. eMarketer estimated that mobile P2P payments will have a transaction volume of over $1 trillion in 2023. While P2P transactions don’t necessarily include merchant relationships, they still make up a critical aspect of the growth of the mobile payment ecosystem.

With P2P payments, through the use of mobile apps, users can enjoy faster and more seamless transactions between two or more people. The security and convenience this offers make P2P a preferred payment method for younger generations. Users can send funds while keeping their bank information private since they only need to provide a phone number or email address.

Buy now, pay later

Buy now, pay later (BNPL) used to be a special offer from merchants, used to entice buyers to make a purchase. More recently, however, it has become a standard offering.

This form of financing works similarly to credit cards, but provides a workaround to lower interest rates and fees, and avoid credit checks. BNPL allows consumers to purchase something they need immediately, while putting off the payment until funds become available.

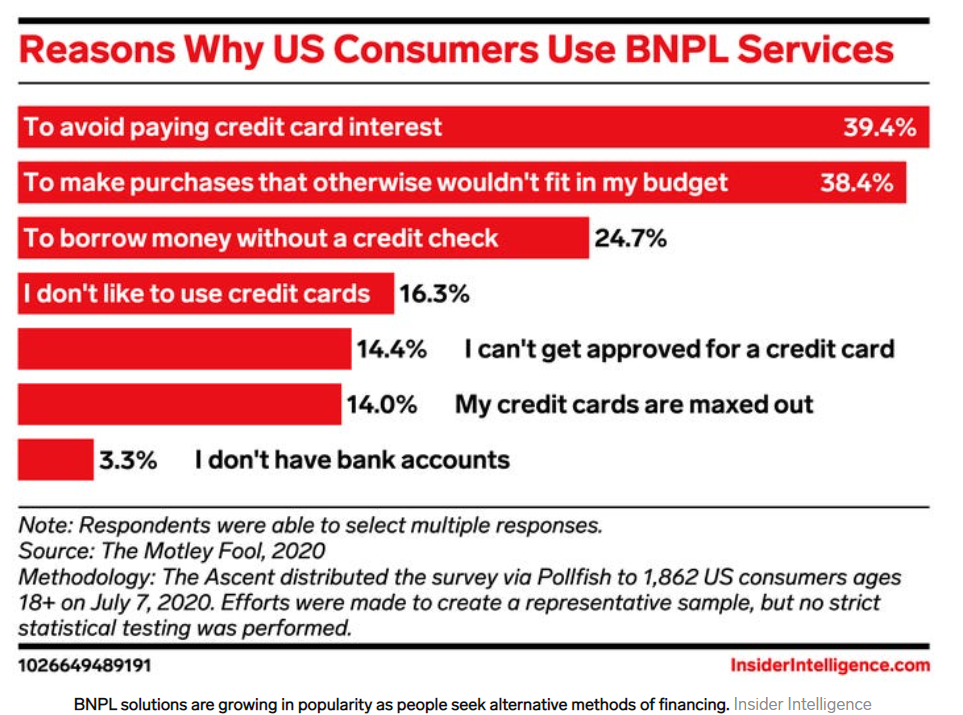

According to Insider Intelligence, the BNPL payment method appeals most to Millennials and Gen Z. However, it’s also widely used among many age groups. As more and more people begin to understand how this payment method works, adoption continues to increase. A survey showed that 62% of BNPL users believe it can become an alternative to using credit cards.

BNPL adoption is still in its early stages. But it’s expected to grow up to 15x its current volume globally by 2025, according to CB Insights.

Cryptocurrency & cross-border digital payments

With the growth of ecommerce, many businesses have gone global, requiring them to activate cross-border payments. These payment methods have intermediaries that often come with high costs.

Transactions performed using traditional methods come with several restrictions, such as limited operating hours and a lack of transparency. Several studies show that using cryptocurrencies for international remittances and payments can help curb fees. A survey by Stellar Development Foundation and Wirex found that 52% of respondents consider cryptocurrencies an excellent alternative to sending money overseas via more traditional methods.

The survey also highlighted that 53% of respondents believe that international fees from traditional payment methods are too steep.

Most global payment systems have high fees and not-so-appealing exchange rates. This can significantly impact the sales and revenue of businesses with international customers.

Since cryptocurrencies run on blockchain technology, they don’t require intermediaries. This effectively lowers transaction fees, allowing transfers to happen in near real-time. Merchants simply have to present their public cryptocurrency wallet address to their customers.

Security through artificial intelligence & machine learning

With the growing popularity of mobile payments, it’s not surprising to see hackers targeting mobile payment users.

A report from NICE Actimize showed that 61% of attempted mobile payment fraud attacks are account takeovers. This is where artificial intelligence (AI) and machine learning (ML) come in. Financial services can identify unusual activity and block suspicious transactions through transaction filtering.

AI technologies and machine learning capabilities can use real-time consumer attributes, such as buying behavior, biometrics, and geolocation, to prevent fraudulent transactions. By using AI and ML, fraud detection becomes more accurate.

Since these systems can interpret data, they help reduce the number of false positives in fraud detection. These systems’ ability to learn over time is also critical for identifying previously undetected tactics used by nefarious individuals.

MPOS technology

As the adoption of mobile payments has become more widespread, the acceptance of mobile point-of-sale (mPOS) technology has also increased. This means that credit card payment processing systems are now also mobile. These devices come with a dedicated wireless system that allows them to function as regular sales terminals and cash registers.

A report by Future Market Insights shows that the mPOS market is expected to reach $140.2 billion within the next 10 years, with a compound annual growth rate (CAGR) of 20.9 percent from 2022 to 2032.

This growth is mainly driven by the flexibility of mPOS technology, which is not only applicable in physical stores, but also in food trucks, trade shows, concerts, fairs, and mobile shops.

Top reasons to use mobile payments

The adoption of mobile payments affords several advantages for both consumers and businesses, including:

Additional security

Mobile phones rid consumers of the need to carry cash and credit cards, which lessens the possibility of these items being stolen. Digital wallets often come with several layers of security before a non-owner can bypass the device.

For example, a mobile wallet may require face recognition or fingerprint technology to open the device and the app itself.

Transactions can have multi-factor authentication before a transfer ensues. Online payments using a mobile device are tokenized. As a result, fraudsters cannot use confidential data when intercepted during the payment process.

Contactless credit card payments use unique identifiers to verify a transaction, preventing hackers from accessing credit card information. Unusual transactions can then be flagged and reversed.

Easier payments for small businesses

P2P payments are not only applicable for splitting bills between friends and family. Small businesses can also use the P2P ecosystem to receive payments for goods and services. These businesses can create a special QR code and post it on their social media channels or share it via mobile phone with their consumers to enable payments.

Speed & efficiency

The payments industry is rapidly changing. Consumers and businesses alike can benefit from the seamless, efficient transactions that mobile payments enable.

Payments are possible with a simple click, tap, or swipe. Businesses also never have to worry about tending loose change, as transactions are always exact. Mobile payment apps can be integrated with financial trackers, allowing for better financial management.

Convenience

Convenience is a major benefit of mobile payment services. For many people, a mobile phone is an everyday companion, used for everything from checking social media accounts to communicating with friends.

Adding mobile payment options allows consumers to have just another function on the mobile device they’re already familiar with.

Mobile payment options indirectly correlate with customer retention. When consumers have control and flexibility over their payment options, this increases buying satisfaction.

Types of mobile payments

With each passing day, more and more businesses are accepting mobile payment options that have passed regulatory compliance by fintech organizations. The following are some of the types of mobile payment methods used today:

In-store payments

In-store payments now go beyond traditional credit and debit cards. Consumers can now also make contactless payments while buying in person. Aside from tap-to-pay contactless credit cards, digital wallets like Apple Pay are also accepted by many brick-and-mortar shops.

Remote payments

Remote payments refer to transactions that happen over the internet. They can be done using a web browser or via a mobile wallet. Most remote payment options have passed regulatory compliance and are highly secure.

Point-of-sale solutions

A point-of-sale payment method that uses NFC technology is another mode of mobile payment. These NFC-enabled card machines can directly communicate with mobile devices as long as they are a few inches away from the terminal.

Empower your business with recurring payment solutions

To stay ahead of the competition and create positive shopping experiences, it’s important to invest in mobile payments. Businesses that maximize partnerships with mobile payment platforms and service providers can improve their brand reputation and gain customer loyalty. Activating contactless cards for in-store payments and mobile wallets for online purchases can help your business stay on top of the competition.

FAQs about mobile payments

What are the risks of using mobile payments?

Mobile payments are not perfect. They come with risks for merchants and consumers, including lost or stolen devices due to factors like weak passwords and human errors. However, these risks are preventable. Several mobile operating systems and applications allow users to wipe out data from stolen devices, preventing further damage.

What’s the future of mobile payments?

The adoption of mobile payment options is likely to increase in the future. More and more, consumers desire flexibility in their payment options, as well as real-time transaction completion, making mobile payments an ideal solution.

What is the most popular type of mobile payment?

As fintech companies continue investing in revolutionizing the financial services space, several payment options are gaining recognition. Some well-known mobile payment providers include PayPal’s Venmo, Apple Pay, Google Pay, and Samsung Pay. In the P2P space, Zelle and Cash App are also gaining popularity among users.